I am sure all of you would have been flooded with news around the changes which have been introduced in the budget by the Finance Minister of India.

This blog should help you in understanding the impact of changes done on Personal Income Tax.

- Tax Exemption upto 7 Lakhs – New Tax Regime

First change introduced is for the tax payers who have adopted the new tax regime, wherein if the taxable income of the tax payer is less than 7 lakh rupees, than no tax will have to be paid by the tax payer. Earlier the same limit was 5 lakh rupees.

For the benefit of individuals who don’t understand what the old and new tax regimes are all about, let me help you understanding the difference.

Under the old tax regime, tax payer’s taxable income is divided into 3 slabs for calculating the tax liability.

Let’s understand this with an example where the taxable amount of a tax payer is 12,50,000 rupees.

So, the total amount of tax to be paid under the old regime would be 1,87,500.

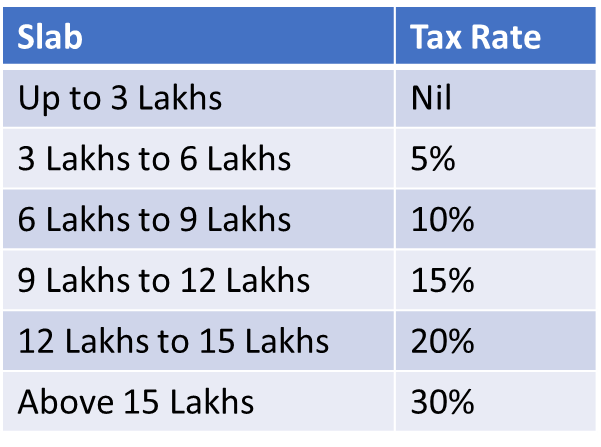

Under the new tax regime, tax payers taxable income is divided into 6 slabs.

Using the example of 12.5 lakhs of taxable income to calculate the tax liability, would result is 1,25,000 rupees of tax liability.

In both old and new tax regime examples, I have ignored the education cess of 4% which is levied on the tax computed as it remains the same across both regimes.

If we now compare the tax liability between both regimes, new tax regime obviously will emerge as a winner where the tax payer will have to pay 62,500 rupees less to the government. So, why should one worry about choosing between old and new tax regime.

One of my good friends used to always use this phrase “The devil is in the details”.

This is where one needs to understand the difference between Income and Taxable Income. In my previous examples, I specifically used the word taxable income. Let’s understand once again with example.

First under the old tax regime, if a tax payer’s Total income is around 17.5 lakhs, tax payer can claim multiple exemptions under different categories to arrive at taxable income. In this example I have considered 5 lakhs as exemption to arrive at taxable income of 12.5 lakhs.

There is an exhaustive list of exemptions, I am naming few here.

- Standard deduction of 50,000 rupees, is available for all salaried and pensioners.

- House Rent Allowance based on few conditions

- Investments done in ELSS mutual funds, Insurance, EPFO or PPF, FD and few other instruments.

- One can even deduct the tuition fees paid for his/her kids.

- Any medical insurance paid for self & family or parents can also be deducted from total income.

- Interest paid towards housing loan upto 2 lakh rupees can also be deducted

Similarly, there are other exemptions which can be claimed on a case by case basis to reduce the income to arrive at taxable income.

Unfortunately, no such exemption was available under the New tax regime. So the total income of an tax payer would remain his taxable income as well.

I hope you now understand the primary difference between old and new tax regimes.

Coming back to the change brought in the budget, tax payers with taxable income upto 7 lakh rupees, will not have to pay any tax under the new tax regime.

However, if an tax payer were to select the old tax regime, tax payer will have to pay tax as per the tax slab old tax regime.

2. Change in Tax Slabs under New Tax Regime

Second change announced is associated with the tax slabs for the new tax regime. There were 6 income tax slabs earlier for New tax regime, which is now reduced to 5 and also the income range is also amended.

Next question which might be coming to your mind is “Did he not say income up to 7 lakh is exempted earlier?” then why is there is a tax slab for 3 to 6 lakhs and 6 to 9 lakhs.

This is where you need to read the lines very carefully. As per the Income tax law if a tax payer’s taxable income under the new regime were to not cross 7 lakhs, then there won’t be any tax liability. But, the moment the taxable income crosses 7 lakhs rupees, this exemption will no longer be applicable and the taxable income will be taxed as per the tax slabs.

3. Standard Deduction for New Tax Regime

As we understood earlier when trying to understand taxable income as per old and new tax regimes, no exemptions were allowed under the new tax regime. So, a tax payer’s total income would eventually be his/her taxable income as well.

In the current budget, tax payers adopting new tax regime are allowed to deduct 50,000 rupees from their total income to arrive at the taxable income.

4. Reduction of Surcharge for New Tax Regime

Fourth change is associated with the surcharge which is charged to high income tax payers. Currently the highest amount of surcharge which the tax payers have to pay is 37% in both old and new tax regimes. Current budget has capped the maximum amount of surcharge to be paid at 25% for tax payers following the new tax regime

5. Leave Encashment Exemption Amendment

Fifth and final change is associated with the amount of money exempted as leave encashment for non-Government salaried employees. Maximum amount of money which was exempted earlier was 3 lakh rupees, which was introduced in 2002 and the same has been now revised to 25 lakhs.

Hope this blog helped you in understanding the changes brought in the budget for 2023-24. Please feel free to reach out to us for any clarification.