If you are reading this article, I am sure you want to know more about this product.

Similar to most of you, I am also a victim of tele marketing (even though my number is registered under the DND list). Tele marketers understand that the initial 10-15 seconds are very crucial to grab the attention of prospective client and they have well written scripts to make the most out of these 10-15 seconds.

This is where the initial question is posed by the tele marketing team:

“Would you be interested in investing in an investment product which will give you guaranteed 12% return?”

Nowadays when Bank FD’s and other fixed income products are delivering around 5.5% to 6% of yearly returns, when we hear about 12% of guaranteed return, most of us would be interested to know further about this product.

As a practicing Certified Financial Planner, I knew that it is a clear case of mis-selling, however I went ahead and requested the tele caller to share more details on, what this product is all about.

Dear readers, please put your seat belts on. You are going to be taken on wonderful drive.

Tele marketing lady proceeded now to explain how 12% is being calculated. To explain this in details, she took the below assumptions:

- Product name is ******* Guaranteed Money Back Plan

- Investor needs to pay a premium of Rs. 1 lakh for 4 years

- Life Insurance cover will be for Rs. 8,52,493

- Investor needs to place a request for surrendering the policy after 4 years

- Upon surrendering the policy, investors would total of 5,35,140 (Breakup provided below)

- Paid Up value – 3,40,997

- Surrender value – 1,94,143

- Upon surrendering the policy, investors would total of 5,35,140 (Breakup provided below)

The next stage is where she made an amazing effort to prove her claim.

Paid Up Value

I was first asked to open the policy terms and conditions wherein, I was directed to the section where it was explained how the paid up policy amount is calculated.

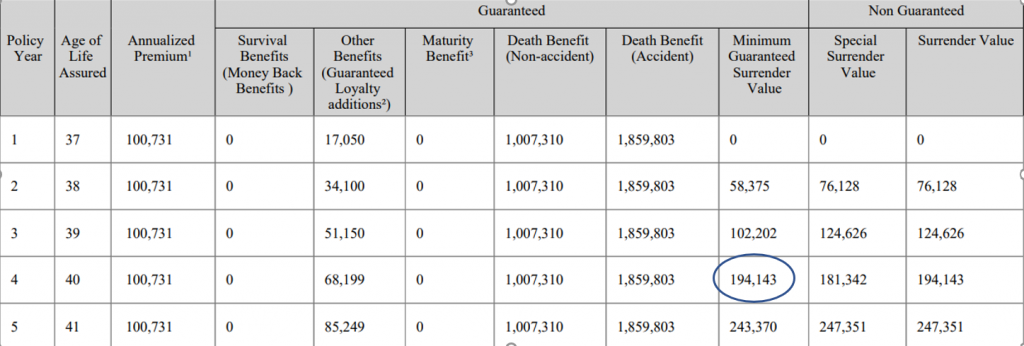

Next, I was guided to generate the illustration of the policy (Below picture for reference) and I was shown that after 4 years, this policy would provide a guaranteed surrender value of Rs.1,94,143.

After summing up both these amounts from Paid up value and Surrender value, I would receive a sum of Rs. 5,35,140 and if we were to calculate the IRR (Internal Rate of Return) with these cashflows, I would see 12%.

This is for the first time, I saw such a detailed effort being made by the tele marketing team in order to prove that their product delivers what was promised in the initial sales pitch.

If a person is not aware of how insurance works, he/she would definitely be convinced with this policy and would be considering buying this policy. However, being a Certified Financial Planner I knew what is wrong and this article is an attempt to explain the same.

Let’s now make an attempt to understand the basics.

What is the definition of a Paid-Up Policy?

In a situation where the investor/insured has paid 2 or more premiums, however he/she is not in a position to pay the remaining premiums, he can request the insurance company to convert his policy into a paid-up policy or even if the insured doesn’t notify the company and fails to make future payments, Insurance company will automatically convert this into a Paid-Up Policy.

When the insurance policy is converted into a Paid-Up Policy, basic sum assured gets reduced with the below formula:

Paid Up Sum Assured = Basic Sum assured X No of Premiums Paid / Total Number of Premiums

Example: If the Basic Sum assured is 10 lakhs, total number of premiums to be paid is 10 but insured has paid 4 premiums then the paid-up sum assured will be Rs. 4 Lakhs (10,00,000 X 4 / 10)

In addition to the paid-up sum assured, loyalty bonus accrued till the paid-up date will be paid in full at the time of policy maturity and also loyalty bonus after the paid-up date is paid on a pro-rata basis based on the paid-up sum assured.

These amounts are paid after the policy tenure is completed and not in the year of discontinuation or surrender as explained by the tele marketing individual, which is completely a false claim.

IRR in this case would be a meagre 4.73% which in simple terms means this policy is failing to beat even the inflation % and other assured fixed income returns.

What is Surrender Value?

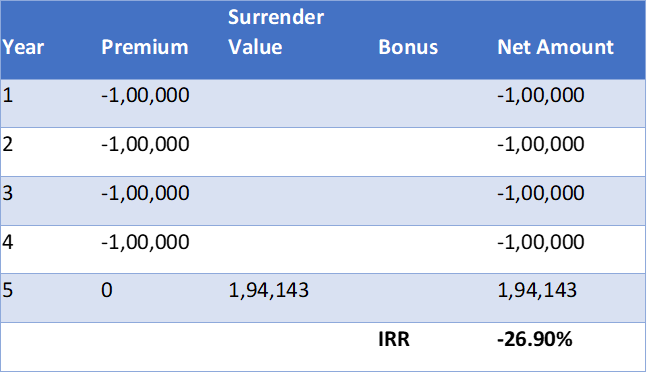

Most of the policies acquires some amount of surrender value after payment of 2 premiums. Surrender value varies for each insurance policy. In this policy, if the insured were to surrender the policy after 4 years, guaranteed surrender value is Rs. 1,94,143.

IRR in this case would be a negative 26.90% which in simple terms means we are going to be losing significant portion of the premiums paid by the insured.

Conclusion

Its either the Paid-up value which is paid on maturity or surrender value if the insured chooses to surrender the policy and both are not paid together. A clear case of mis-representation of facts by the tele marketing individual.

If you pay 1 premium and do not return it during the free look up period, you will find it very hard to convince yourself that you are going to lose a significant portion of the premium paid and you will end up continuing to pay premiums for such policies till maturity (Here I am speaking out of experience after assisting 85 families, we have seen quite a lot such instances)

Please be cautious about such tele marketing calls and do not fall prey to such mis-selling. Its always better to “Shout in Doubt”. Seeking an expert opinion before subscribing for any such policy would be a wise choice.

We would be more than happy to help you in making the right choice without any obligation to purchase from us. Remember we are just an email or a call away.

Disclaimer: Above published information is for education purpose only and the views expressed by the author is bases on his personal experience and knowledge. Please consult your Certified Financial Planner before taking any financial decision.