What is super top up policy in health insurance?

Have you heard of Super Top Up Health Insurance policies which can provide medical cover up to 50 lakhs, at a cost of less than 10 rupees per day. This is cheaper than the amount of money people spend for a cup of coffee or tea. If you want to know more about this policy, please spare few minutes to read this article on Super Top Up Health Policy. Few minutes of your time can help you in saving several lakhs of your hard earned money in future.

Most of us are aware of the benefits of having a medical insurance policy, but not many are aware of Super Top up health Insurance policy and its benefits, as this is now widely marketing by the insurance companies.

These policies provide huge amount of coverage to the insured while being very light on the pocket. If we were to look at a cover of 50 lakhs for an individual of 35 years of age, annual premium will be around Rs. 3,500 which translates to less than 10 rupees per day.

Concept of Deductible in Super Top Up Health Policy

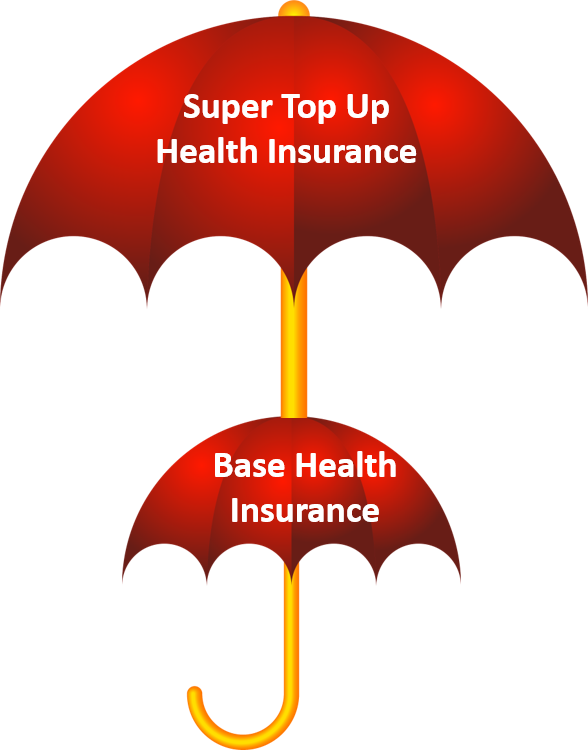

While the Base insurance policy for 5 lakhs for the same individual costs around Rs. 8,500 per annum, why do you think the super top up medical policy providing a cover of 50L is so economical?

Answer to that question is the concept of deductible. All Super Top Up health policies have this concept of deductible wherein a certain sum of money will not be paid by these policies.

Let’s understand this with an example where the insured has availed a Super Top Up Policy for 50 lakhs with deductible of 5 lakhs.

If the Hospital bill turns out to be 20 lakhs, initial 5 lakh rupees will not be paid by the super top up policy and the same needs to be borne by the insured through his base insurance policy or employer provided medical policy or from his/her pocket.

| Hospital Bill | 20,00,000 |

| Deductible – Not paid by Super Top Up Policy | 5,00,000 |

| Claim amount paid by Super Top Up Policy | 15,00,000 |

Any amount over and above 5L will be settled by this policy up to the sum insured. In this case 15 lakh rupees will be paid towards hospitalization expense.

This is a must buy product for every family, as it provides enough cover to the whole family in case of any health issues. Availing this policy will lay a strong foundation for achieving your financial goals as most of the medical emergencies will be taken care of by this policy.

This policy can be either availed individually or as family floater (will help in reducing the premiums).

Top Up Health Policy Vs Super Top Up Health Policy

Once you decide to buy the super top up product and go to any medical insurer website you might be given 2 options to choose from i.e.,

- Whether you want to buy a Top Up Policy or

- Super Top Up policy

Basic concept remains the same in both the policies i.e., initial deductible will not be paid and you will have cover over and above the deductible amount specified.

But there is a small difference on how deductible is considered, which can create a huge impact on the claim settlement amount.

Example

Example Explained

Lets assume the policy sum assured is for 50 lakhs and deductible is 5 lakhs for both types of policies.

During the policy year, first claim is for 4.5 lakh. As the claim amount is less than the deductible amount, no amount will be paid under both type of policies.

During the same policy year, when there is a second claim for 6 lakhs, Top Up policy will provide an amount of 1 lakh towards the claim, whereas super top up policy will pay you an amount of 5.5 lakh rupees.

Why do you think there such a variance in the claims paid by both the policies.

If you haven’t realized the reason, let me explain it. Under Top Up policies, deductible is applied for each and every medical claim. Only after the deductible amount is crossed, top up policy will be liable to pay the insured.

In case of Super Top Up Policy, every hospitalization expense incurred by the insured during the policy year is summed together to consider the deductible amount i.e., in this example first claim of 4.5 lakhs plus current claim of 6 lakhs will be added together resulting in 10.5 lakhs and from this 5 lakhs will be deducted and insurance claim of 5.5 lakhs will be paid to the insured.

Conclusion

Premium difference between both types of policies will be hardly few hundreds, however, if you don’t understand the product then you will end up losing huge amount of money during claim period.

Please ensure you read the policy wordings of any health insurance policy carefully before purchasing the product. If you want to take professional assistance in availing medical insurance cover for yourself and your family, we are just a phone call away or leave us your contact details and we will get in touch with you.

Please join me in my effort to spread financial literacy and share this post with your friends and family.